After studying this section, students should be able to do the following:

Budget decisions are affected by conditions both internal and external to the client. One key external influence is the overall economic condition of the country and how this affects the client’s industry. Even the most inspired advertising may not motivate consumers to open their wallets in troubled times like now. We see this situation now quite clearly, for example, in the automotive industry, as the stock market and credit crises have made money scarce, and consumers are pressed to pay higher prices for gasoline, home heating, groceries, and other necessities. It’s not surprising, then, that automotive advertising spending in the United States dropped to $1.99 billion in the first quarter of 2008. That sounds like a lot of money (and it is!)—but it’s down more than 14 percent compared with the same time a year before. As one industry executive observed, ad spending is “sinking as fast as new car sales.” When times are tough, nothing is sacred: Even Tiger Woods’ nine-year relationship as a fixture in General Motors’ advertising got the axe as the industry tries to slash its costs.Quoted in “Auto Ad Spending Down, Except Digital,” eMarketer, July 23, 2008, http://www.emarketer.com/Article.aspx?id=1006426&src=article1_newsltr (accessed July 23, 2008); Rich Thomaselli, “GM Ending Tiger Woods Endorsement Deal,” Advertising Age, November 24, 2008, http://adage.com/article?article_id=132810 (accessed November 28, 2008); http://adage.com/article?article_id=46288& search_phrase=shona%20seifert.

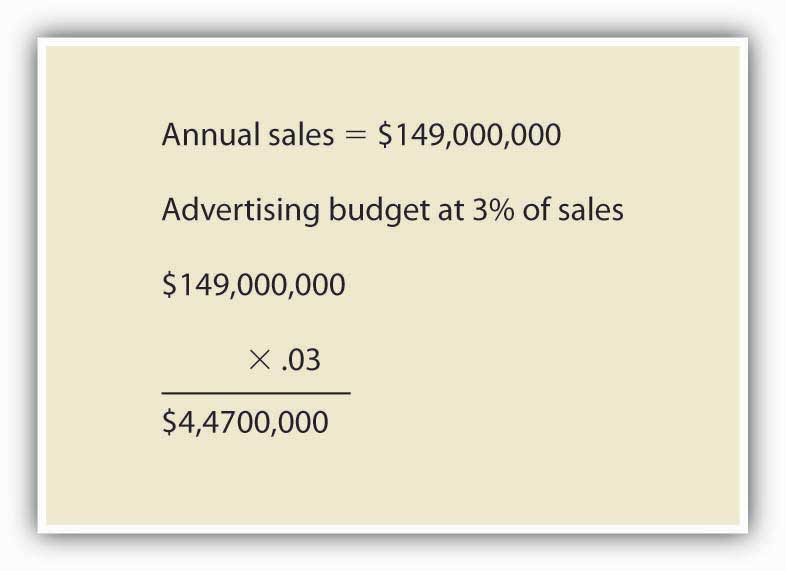

In top-down budgetingMethod in which top management sets the amount the company will spend on promotional activities for the year; it is allocated among all of the company’s advertising, PR, and other promotional programs., top management sets the overall amount the company will spend on promotional activities for the year. This total amount is then allocated among all of the advertising, PR, and other promotional programs. How does top management arrive at the annual promotional budget? Typically, they use a percentage-of-sales method, in which the budget is based on the amount the company spent on advertising in the previous year and the sales in that year.

The percentage-of-salesBudgeting method that divides the ratio of the firm’s past annual promotional budget by past sales to arrive at the percentage of sales; this is applied to expected sales in the coming year to arrive at the ad budget for that year. method is the ratio of the firm’s past annual promotional budget divided by past sales to arrive at the percentage of sales. That percentage of sales is then applied to the expected sales in the coming year to arrive at the budget for that year. For example, if the company spent $20 million on advertising last year and had $100 million in sales, the percentage of sales would be 20 percent. If the company expects to achieve $120 million in sales the following year, then 20 percent of $120 million is $24 million, which would be the budget for advertising that year.

Figure 7.2 Percentage-of-Sales Method

Wall Street analysts sometimes look at changes in the ad-to-sales ratioThe relationship between a company’s promotional budget and its sales; this ratio is important to business analysts in assessing a company’s health. as a sign of the health of a company. For example, Procter & Gamble’s ad-to-sales-ratio slipped from 10.7 percent in 2004 to 9.9 percent in 2006. Those declines came as P&G faced growing margin pressure from rising commodity costs. Some analysts see strong ad spending as an investment in growth or a sign that a company is having no trouble meeting its earnings targets, so they want to see an ad-to-sales ratio that is consistent or increasing.Jack Neff, “P&G Rewrites its Definition of ‘Ad Spend,’” Advertising Age, September 3, 2007, 3.

Some companies use industry averagesA technique for evaluating ad-to-sales ratios based on the ratios seen in a group of companies in a given industry. (published by trade associations) as a guide to set their promotional budget. Ad-to-sales ratios vary widely depending on the industry. For example, health services companies had one of the highest ad-to-sales ratios for 2006, at 18.7 percent. Other industries with high ad-to-sales ratios are transportation services (14.2 percent), motion pictures and videotape productions (13.7 percent), food (11.9 percent), newspapers (11.1 percent), and broadcast television stations (10.7 percent). In contrast, computer and office equipment had an ad-to-sales ratio of 1.2 percent, while computers and software wholesale had only a 0.2 percent ad-to-sales ratio.Kate Maddox, “Ad Spending Up in ’05, ’06,” B to B, August 8, 2005, 17.

Sometimes a dramatic increase in ad spending by one competitor in an industry spurs others to follow suit. For example, in 2007 German insurance giant Allianz more than quadrupled its annual global advertising budget to 225 million euros after competitor Zurich Financial Services launched a large-scale global awareness campaign.“Allianz Plans €225m Global Branding Blitz,” Marketing Week, May 3, 2007, http://goliath.ecnext.com/coms2/gi_0199-6503373/Allianz-plans-225m-global-branding.html (accessed February 1, 2009). Similarly, the auto insurance industry saw overall ad spending jump more than 32 percent in just two years when GEICO increased its ad spending 75 percent in 2004; this spurred competitors to increase their ad budgets as well. Progressive Insurance spent $265 million in 2006, up from $201 million in 2004, and State Farm likewise plans to increase spending, which topped $270 million in measured media in 2006.Mya Frazier, “Geico’s $500M Outlay Pays Off,” Advertising Age, July 9, 2007, 8.

Spending on certain segments of the promotional budget, such as on coupons, is very much driven by competitor spending levels. Consumer packaged goods companies like P&G and Unilever claim not to like couponing schemes as a promotional activity. Indeed, P&G looked into eliminating coupons in 1997 due to declining newspaper circulation and usage. But companies are tied to using coupon promotions. If one company alone decides to forgo couponing, they face losing cost-conscious consumers to the competition. If companies try to work together to scale back on couponing, they might be accused of violating antitrust regulations. As a result, spending on the media side of couponing was up 26 percent in 2006, reaching $1.8 billion, even though consumer use of coupons was down 13 percent during the same time period.Jack Neff, “Package-Goods Players Just Can’t Quit Coupons,” Advertising Age, May 14, 2007, 8.

The advantages of top-down approaches are their speed and straightforwardness. The disadvantage is that the methods look to the past as a guide, rather than to future goals. Just because a company spent $40 million on advertising the previous year doesn’t mean that figure is right for next year. Also, budgets tied to sales figures mean that a company’s promotional budget will decrease if sales decrease—but in fact increasing the promotional budget may be precisely what is needed in order to remedy declining sales.

Alternatively, some companies begin the budgeting process each year with a clean slate. They use bottom-up budgetingMethod in which a company begins the promotional budgeting process each year with a clean slate, identifying promotional goals and allocating enough money to achieve those goals. techniques, in which they first identify promotional goals (regardless of past performance) and allocate enough money to achieve those goals.

The objective-task methodThe most common technique of bottom-up budgeting, in which a company sets the objective or task they want the promotion to achieve, then estimates the budget needed to achieve it; top management reviews and approves the budget recommendation. is the most common technique of bottom-up budgeting. Companies that use this method first set the objective or task they want the promotion to achieve. Next, they estimate the budget they will need to accomplish that objective or task. Finally, top management reviews and approves the budget recommendation.

For example, champagne maker Moët & Chandon set its objective “to grow the whole market” in the United States.Jeremy Mullman, “Moët, Rivals Pour More Ad Bucks into Bubbly: Champagne Makers Try to Create Year-Round Demand,” Advertising Age, September 3, 2007, 4. That is, Moët will use advertising to increase consumption of champagne throughout the year, not just over the holidays. Moët based its objective on research that compared champagne consumption in the United States to that in other countries. “The average U.S consumer drinks half a glass of champagne a year, the average British consumer drinks half a bottle and the average French consumer drinks three bottles. There’s clearly room for growth,” said Stuart Foster, director of business development at Moët-Hennessy USA.Jeremy Mullman, “Moët, Rivals Pour More Ad Bucks into Bubbly: Champagne Makers Try to Create Year-Round Demand,” Advertising Age, September 3, 2007, 4. Moët more than tripled its U.S. ad spending in 2006 to $9.5 million from $2.8 million. Reflecting the objective, the company ran its advertising in the summer rather than just around the holidays.

Similarly, Danone Waters is increasing its ad spending in the United Kingdom in 2008 in an effort to increase bottled water consumption among British consumers. Danone Waters is increasing its spending by 15 percent, compared to Moët’s tripling of ad expenditures, which shows that there is no hard-and-fast rule about how much budget is needed to reach a given objective.Jeremy Mullman, “Moët, Rivals Pour More Ad Bucks into Bubbly: Champagne Makers Try to Create Year-Round Demand,” Advertising Age, September 3, 2007, 4; “Danone Waters Plans to Increase Spend by 15%,” Marketing, July 25, 2007, 4.

Other objectives advertisers can set include acquiring new customers, retaining existing customers, or building the brand. The objective to acquire new customers often requires a bigger budget than the advertising the firm needs to retain existing customers.

Some companies use the product life cycle methodStage-based budgeting technique that allocates more money during the introduction stage of a new product than in later stages when the product is established., in which they allocate more money during the introduction stage of a new product than in later stages when the product is established. For example, Procter & Gamble allocated $15 million to advertising Dawn Simple Pleasures, a new liquid detergent product that comes with a separate air freshener attached to the base of the bottle. It allocated less money ($10–12 million) for Dawn Direct Foam, a product it launched two years prior.Vanessa L. Facenda, “Procter Dishes out 3-Tiered Dawn Attack,” Brandweek, September 24, 2007, 4. The need to spend heavily to promote new products is especially strong for pharmaceutical companies when they introduce new drugs. Pharmaceutical companies need to get physicians to talk about their drugs and prescribe them.

In contrast, companies such as baby food manufacturers need to invest in strong promotion on a continual basis, because they get a new set of customers every year. “We provide strong consumer promotion support to drive trial, particularly in our baby segments, where we have a new group of consumers entering the market each year,” said Randy Sloan, executive vice president and general manager at Del Pharmaceuticals, which is the number one advertiser in teething pain relief, children’s toothpaste, and adult oral pain products.Quoted in “A Targeted Approach Creates a Powerhouse,” Chain Drug Review, June 4, 2007, 34.

Since msnbc.com’s fiscal year runs from July to June, Catherine Captain and all other department heads must start submitting their budget requests in March so that the board can determine their budgets before the next fiscal year starts. They use a bottom-up strategy based on objectives, but sales are also a vital part of determining what the final spend will be.

Catherine Captain

(click to see video)Catherine Captain talks about the relativity of budget sizes.

In addition to deciding how much to spend, companies need to know when they will be spending the money.

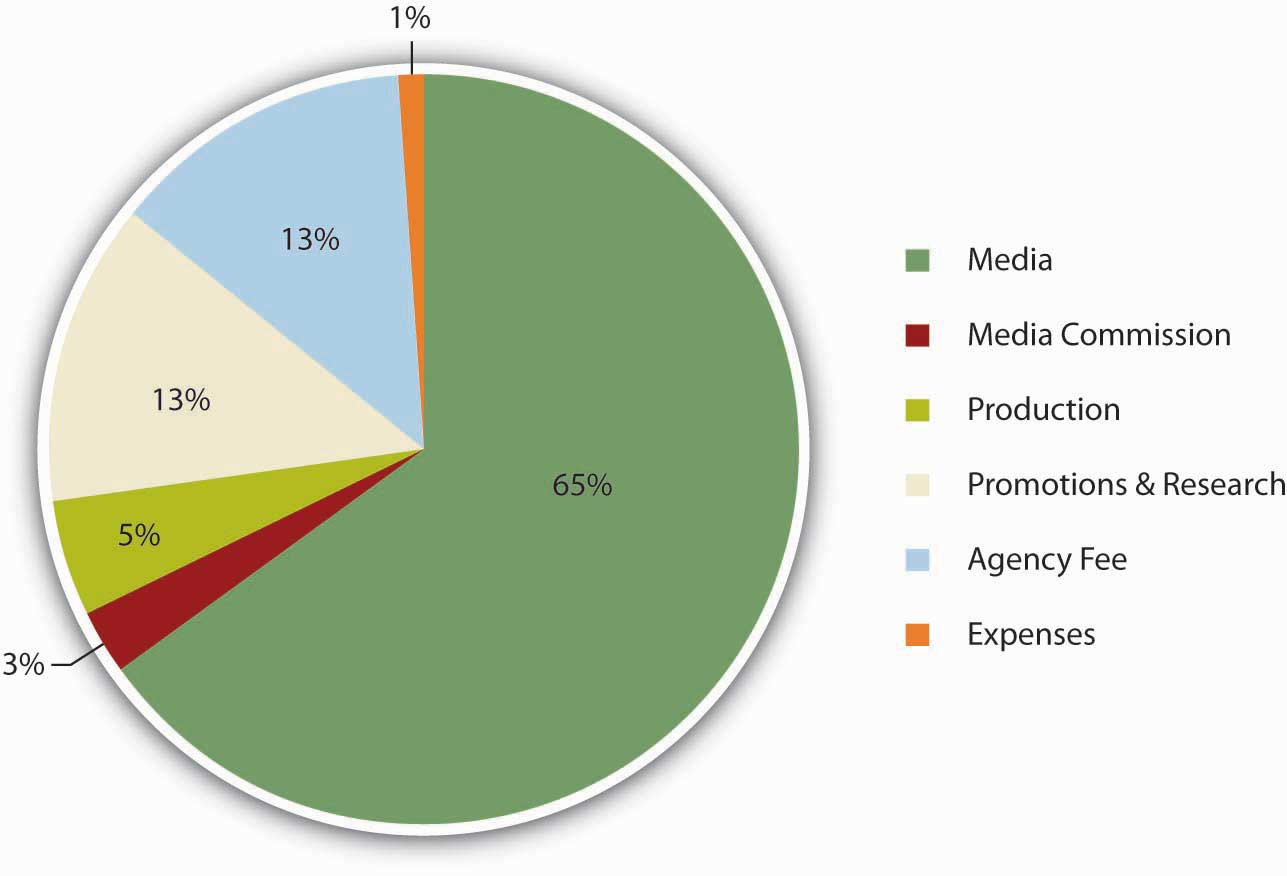

Figure 7.3 msnbc.com Budget Allocation

For some companies, the timing is smooth. As we saw with the Moët champagne example, the company will spend its budget throughout the year. Many other businesses step up their advertising in the weeks leading up to the Christmas holiday season. Others, such as beach apparel makers or home improvement companies whose work is done in warm weather, may concentrate their spending during a particular time of year.

Keep in mind that the budget needs to pay for more than just creating the ads and buying the media to run them. Consider a beachwear campaign for an apparel maker as an example. Although most of the campaign budget is spent in the second quarter on media buys to hit consumers with swimsuit ads as they gear up for summer, the ad agency has to allocate some of the money to laying the groundwork for this campaign. It will need to spend some money in the earlier part of the year to pay for market research, ad development, and testing. After the ads run, the last of the budget might go to assess the campaign’s effectiveness.

Other factors that contribute to budgeting:

While a lump sum budget had been approved for SS+K to spend, Catherine Captain and msnbc.com had to be responsive to their internal revenue situations. In other words, if they weren’t hitting other advertising sales objectives, they were not going to be ready to pull the trigger on the disbursement of millions of dollars.

Figure 7.4 Budget Snapshot of the Elements and Timing for the msnbc.com Campaign

SS+K outlined each element of the production and when the agency would have to have the client’s money fully committed and available to spend. Part of the account management team’s responsibility is to manage the schedule by which everyone gets paid for her part in a production.

Catherine Captain

(click to see video)Catherine Captain explains the importance of the first marketing budget and what would happen if it didn’t go well.

Clients use a variety of methods to determine their advertising budgets. One basic distinction is between top-down and bottom-up methods. Top-down approaches are easier; they basically use last year’s expenditures as a starting point. However, they also are more simplistic and may be self-defeating because they wind up allocating more money to promote products that are doing well at the expense of products that are doing poorly—when just the opposite adjustment may make more sense. Bottom-up approaches start by specifying the particular objectives a firm has for a brand and then estimating how much it will cost to meet those objectives. Budget-setting is more complicated than just tallying up what it costs to make and place advertising; the client also has to consider the resources an agency will need to conduct research, develop an advertising strategy, and measure how well the strategy worked so it can tweak the approach in the future if necessary.