This chapter has focused on performing variance analysis to evaluate and control operations. Standard costing systems assist in this process and often involve recording transactions using standard cost information. When accountants use a standard costing system to record transactions, companies are able to quickly identify variances. In addition, inventory and related cost of goods sold are valued using standard cost information, which simplifies the bookkeeping process.

Question: In Figure 10.4 "Direct Materials Variance Analysis for Jerry’s Ice Cream", we calculated two variances for direct materials at Jerry’s Ice Cream: materials price variance and materials quantity variance. How are these variances recorded for transactions related to direct materials?

Answer: Two journal entries are needed to record direct materials transactions that include these variances. An example of each is shown next. (Typically, many more journal entries would be made throughout the year for direct materials. For the purposes of this example, we will make one journal entry for each variance to summarize the activity for the year.)

The entry to record the purchase of direct materials and related price variance shown in Figure 10.4 "Direct Materials Variance Analysis for Jerry’s Ice Cream" is

Notice that the raw materials inventory account contains the actual quantity of direct materials purchased at the standard price. Accounts payable reflects the actual cost, and the materials price variance account shows the unfavorable variance. Unfavorable variances are recorded as debits and favorable variances are recorded as credits. Variance accounts are temporary accounts that are closed out at the end of the financial reporting period. We show the process of closing out variance accounts at the end of this appendix.

The entry to record the use of direct materials in production and related quantity variance shown in Figure 10.4 "Direct Materials Variance Analysis for Jerry’s Ice Cream" is

Work-in-process inventory reflects the standard quantity of direct materials allowed at the standard price. The reduction in raw materials inventory reflects the actual quantity used at the standard price, and the materials quantity variance account shows the favorable variance.

Question: In Figure 10.6 "Direct Labor Variance Analysis for Jerry’s Ice Cream", we calculated two variances for direct labor at Jerry’s Ice Cream: labor rate variance and labor efficiency variance. How are these variances recorded for transactions related to direct labor?

Answer: Because labor is not inventoried for later use like materials, only one journal entry is needed to record direct labor transactions that include these variances. (Again, many more journal entries would typically be made throughout the year for direct labor. For the purposes of this example, we will make one journal entry to summarize the activity for the year.)

The entry to record the cost of direct labor and related variances shown in Figure 10.6 "Direct Labor Variance Analysis for Jerry’s Ice Cream" is

Work-in-process inventory reflects the standard hours of direct labor allowed at the standard rate. The labor rate and efficiency variances represent the difference between work-in-process inventory (at the standard cost) and actual costs recorded in wages payable.

Question: As discussed in Chapter 2 "How Is Job Costing Used to Track Production Costs?", the manufacturing overhead account is debited for all actual overhead expenditures and credited when overhead is applied to products. At the end of the period, the balance in manufacturing overhead, representing overapplied or underapplied overhead, is closed out to cost of goods sold. This overapplied or underapplied balance can be explained by combining the four overhead variances summarized in this chapter in Figure 10.14 "Comparison of Variable and Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream". How are these variances recorded for transactions related to manufacturing overhead?

Answer: Based on the information at the left side of Figure 10.14 "Comparison of Variable and Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream", the entry to record actual overhead expenditures is

The credit goes to several different accounts depending on the nature of the expenditure. For example, if the expenditure is for indirect materials, the credit goes to accounts payable. If the expenditure is for indirect labor, the credit goes to wages payable.

The next entry reflects overhead applied to products. This information comes from the right side of Figure 10.14 "Comparison of Variable and Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream".

At this point, manufacturing overhead has a $16,000 credit balance, which represents overapplied overhead ($16,000 = $252,000 applied overhead – $236,000 actual overhead). The following summary of fixed and variable overhead variances shown in Figure 10.14 "Comparison of Variable and Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream" explains the overapplied amount of $16,000:

Question: Review all the debits to work-in-process inventory throughout this appendix and you will see the following costs (all recorded at standard cost):

How are these costs transferred from work-in-process inventory to finished good inventory when the goods are completed?

Answer: When the 210,000 units are completed, the following entry is made to transfer the costs out of work-in-process inventory and into finished goods inventory.

Note that the standard cost per unit was established at $4.50, which includes variable manufacturing costs of $3.80 (see Figure 10.1 "Standard Costs at Jerry’s Ice Cream") and fixed manufacturing costs of $0.70 (see footnote to Figure 10.12 "Fixed Manufacturing Overhead Information for Jerry’s Ice Cream"). Total production of 210,000 units × Standard cost of $4.50 per unit equals $945,000; the same amount you see in the entry presented previously.

Question: How do we record the costs associated with products that are sold?

Answer: When finished product is sold, the following entry is made:

Note that the entry shown previously uses standard costs, which means cost of goods sold is stated at standard cost until the next entry is made.

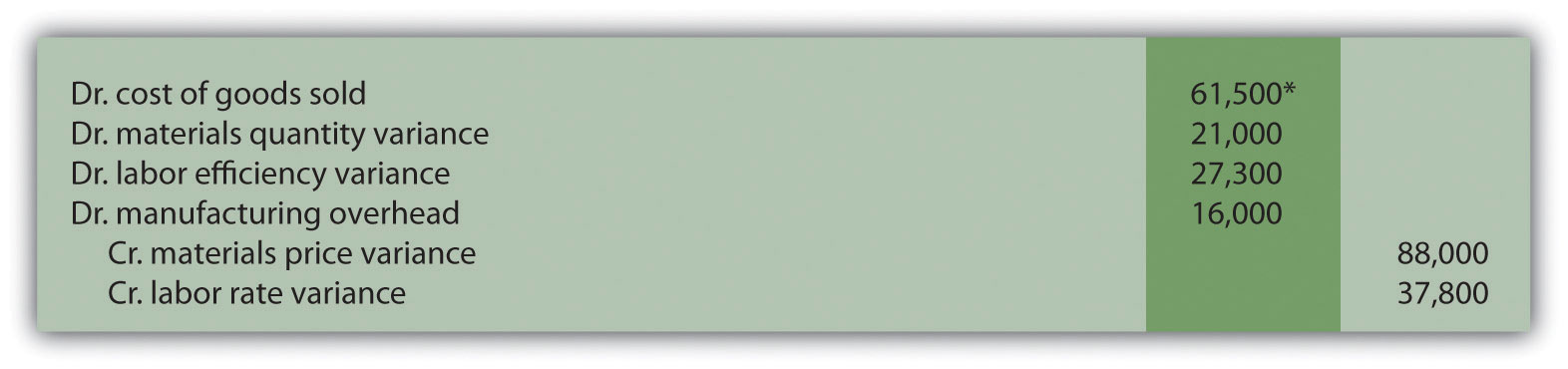

Question: At the end of the period, Jerry’s Ice Cream has balances remaining in manufacturing overhead along with all the variance accounts. These accounts must be closed out at the end of the period. How is this accomplished?

Answer: These accounts are closed out to cost of goods sold, after which point cost of goods sold will reflect actual manufacturing costs for the products sold during the period. The following entry is made to accomplish this goal:

*$61,500 = $88,000 + $37,800 – $21,000 – $27,300 – $16,000.

Solution to Review Problem 10.9

The following is a journal entry to record purchase of raw materials:

The following is a journal entry to record usage of raw materials:

The following is a journal entry to record direct labor costs:

The following is a journal entry to record actual overhead expenditures:

The following is a journal entry to record overhead applied to production:

The product cost data recorded in work-in-process inventory for the period is as follows:

Thus the journal entry to transfer these production costs from work in process to finished goods is:

The following is a journal entry to record transfer of finished goods to cost of goods sold:

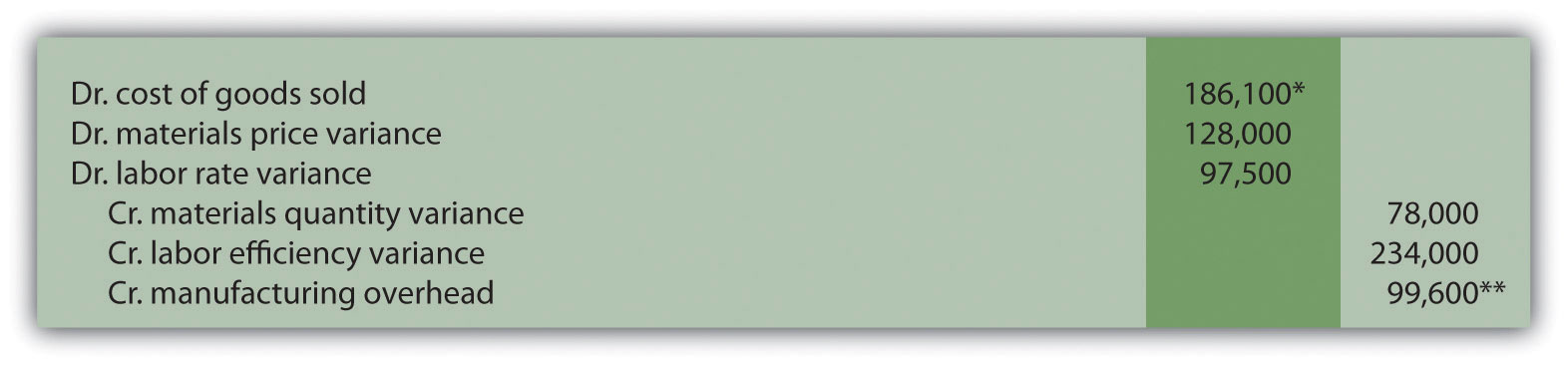

The following is a journal entry to close out manufacturing overhead and all variance accounts:

*$186,100 = $78,000 + $234,000 + $99,600 – $128,000 – $97,500.

**$99,600 underapplied overhead = $630,000 actual overhead costs – $530,400 applied overhead. Because this represents a debit balance in manufacturing overhead, the account must be credited to close it. To further prove this is accurate, the sum of all overhead variances must equal $99,600 unfavorable as shown in the following:

| Variable overhead spending variance | $18,750 unfavorable (from Note 10.49 "Review Problem 10.5") |

| Variable overhead efficiency variance | $68,250 unfavorable (from Note 10.49 "Review Problem 10.5") |

| Fixed overhead spending variance | $5,340 unfavorable (from Note 10.67 "Review Problem 10.8") |

| Fixed overhead production volume variance | $7,260 unfavorable (from Note 10.67 "Review Problem 10.8") |

| Total manufacturing overhead variance | $99,600 unfavorable |

Questions

Brief Exercises

Exercises: Set A

Standard Cost and Flexible Budget. Hal’s Heating produces furnaces for commercial buildings. The company’s master budget shows the following standards information.

| Expected production for January | 300 furnaces |

| Direct materials | 3 heating elements at $40 per element |

| Direct labor | 35 hours per furnace at $18 per hour |

| Variable manufacturing overhead | 35 direct labor hours per furnace at $15 per hour |

Required:

Materials and Labor Variances. Hal’s Heating produces furnaces for commercial buildings. (This is the same company as the previous exercise. This exercise can be assigned independently.)

For direct materials, the standard price for a heating element part is $40. A standard quantity of 3 heating elements is expected to be used in each furnace produced. During January, Hal’s Heating purchased 1,000 heating elements for $38,000 and used 980 heating elements to produce 320 furnaces.

For direct labor, Hal’s Heating established a standard number of direct labor hours at 35 hours per furnace. The standard rate is $18 per hour. A total of 10,000 direct labor hours were worked during January, at a cost of $190,000, to produce 320 furnaces.

Required:

Variable Overhead Variances. Hal’s Heating produces furnaces for commercial buildings. (This is the same company as the previous exercises. This exercise can be assigned independently.) The company applies variable manufacturing overhead at a standard rate of $15 per direct labor hour. The standard quantity of direct labor is 35 hours per unit. Variable overhead costs totaled $190,000 for the month of January. A total of 10,000 direct labor hours were worked during January to produce 320 furnaces.

Required:

Calculate the variable overhead spending variance and variable overhead efficiency variance using the format shown in Figure 10.8 "Variable Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream". Clearly label each variance as favorable or unfavorable.

Fixed Overhead Variance Analysis. Hal’s Heating produces furnaces for commercial buildings. (This is the same company as the previous exercises. This exercise can be assigned independently.) The company applies fixed manufacturing overhead costs to products based on direct labor hours. Information for the month of January appears as follows. Hal’s expected to produce and sell 300 units for the month.

Required:

Calculate the fixed overhead spending variance and production volume variance using the format shown in Figure 10.13 "Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream". Clearly label each variance as favorable or unfavorable.

Journalizing Direct Materials and Direct Labor Transactions (Appendix). Hal’s Heating produces furnaces for commercial buildings. (This is the same company as the previous exercises. This exercise can be assigned independently.)

Direct materials and direct labor variances for the month of January are shown as follows.

| Materials price variance | $(2,000) favorable |

| Materials quantity variance | $ 800 unfavorable |

| Labor rate variance | $ 10,000 unfavorable |

| Labor efficiency variance | $(21,600) favorable |

Required:

Investigating Variances. Quality Tables, Inc., produces high-end coffee tables. Standard cost information for each table is presented as follows.

Quality Tables produced and sold 2,000 tables for the year and encountered the following production variances:

Required:

Company policy is to investigate all unfavorable variances above 10 percent of the flexible budget amount for direct materials, direct labor, and variable overhead.

Variance Analysis with Activity-Based Costing. Assume Mammoth Company uses activity-based costing to allocate variable manufacturing overhead costs to products. The company identified three activities with the following information for last quarter.

| Activity | Standard Rate | Standard Quantity per Unit Produced | Actual Costs | Actual Quantity |

| Indirect materials | $2.40 per yard | 7 yards per unit | $691,650 | 265,000 yards |

| Product testing | $1.50 per test minute | 5 minutes per unit | $301,000 | 215,000 test minutes |

| Indirect labor | $4.50 per direct labor hour | 4 hours per unit | $930,000 | 180,000 direct labor hours |

Required:

Assume Mammoth Company produced 40,000 units last quarter. Prepare a variance analysis using the format shown in Figure 10.11 "Variable Overhead Variance Analysis for Jerry’s Ice Cream Using Activity-Based Costing". Clearly label each variance as favorable or unfavorable.

Closing Variance and Overhead Accounts (Appendix). Gonzaga Products had the following balances at the end of its fiscal year.

| Debit | Credit | |

| Materials price variance | $10,000 | |

| Materials quantity variance | $8,000 | |

| Labor rate variance | 6,000 | |

| Labor efficiency variance | 5,000 | |

| Manufacturing overhead | 14,000 |

Required:

Exercises: Set B

Standard Cost and Flexible Budget. Outdoor Products, Inc., produces extreme-weather sleeping bags. The company’s master budget shows the following standards information.

| Expected production for September | 5,000 units |

| Direct materials | 8 yards per unit at $5 per yard |

| Direct labor | 3 hours per unit at $16 per hour |

| Variable manufacturing overhead | 3 direct labor hours per unit at $2 per hour |

Required:

Materials and Labor Variances. Outdoor Products, Inc., produces extreme-weather sleeping bags. (This is the same company as the previous exercise. This exercise can be assigned independently.)

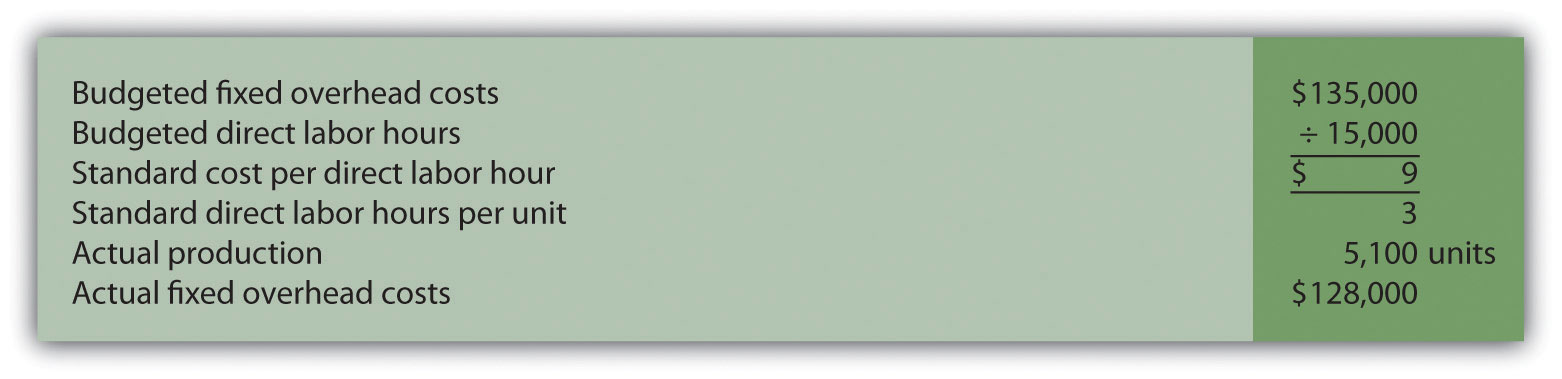

For direct materials, the standard price for 1 yard of material is $5 per yard. A standard quantity of 8 yards of material is expected to be used for each sleeping bag produced. During September, Outdoor Products, Inc., purchased 45,000 yards of material for $238,500 and used 39,000 yards to produce 5,100 sleeping bags.

For direct labor, Outdoor Products, Inc., established a standard number of direct labor hours at three hours per sleeping bag. The standard rate is $16 per hour. A total of 14,700 direct labor hours were worked during September, at a cost of $238,140, to produce 5,100 sleeping bags.

Required:

Variable Overhead Variances. Outdoor Products, Inc., produces extreme-weather sleeping bags. (This is the same company as the previous exercises. This exercise can be assigned independently.) The company applies variable manufacturing overhead at a standard rate of $2 per direct labor hour. The standard quantity of direct labor is three hours per unit. Variable overhead costs totaled $32,000 for the month of September. A total of 14,700 direct labor hours were worked during September to produce 5,100 sleeping bags.

Required:

Calculate the variable overhead spending variance and variable overhead efficiency variance using the format shown in Figure 10.8 "Variable Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream". Clearly label each variance as favorable or unfavorable.

Fixed Overhead Variance Analysis. Outdoor Products, Inc., produces extreme-weather sleeping bags. (This is the same company as the previous exercises. This exercise can be assigned independently.) The company applies fixed manufacturing overhead costs to products based on direct labor hours. Information for the month of September appears as follows. Outdoor Products expected to produce and sell 5,000 units for the month.

Required:

Calculate the fixed overhead spending variance and production volume variance using the format shown in Figure 10.13 "Fixed Manufacturing Overhead Variance Analysis for Jerry’s Ice Cream". Clearly label each variance as favorable or unfavorable.

Journalizing Direct Materials and Direct Labor Transactions (Appendix). Outdoor Products, Inc., produces extreme-weather sleeping bags. (This is the same company as the previous exercises. This exercise can be assigned independently.)

Direct materials and direct labor variances for the month of September are shown as follows.

| Materials price variance | $13,500 unfavorable |

| Materials quantity variance | $(9,000) favorable |

| Labor rate variance | $ 2,940 unfavorable |

| Labor efficiency variance | $(9,600) favorable |

Required:

Investigating Variances. Tool Box, Inc., produces tool boxes sold at a variety of retail stores throughout the world. Standard cost information for each toolbox is presented as follows.

Tool Box produced and sold 100,000 toolboxes for the year and encountered the following production variances:

Required:

Company policy is to investigate all unfavorable variances above 5 percent of the flexible budget amount for direct materials, direct labor, and variable overhead.

Variance Analysis with Activity-Based Costing. Assume Hillside Hats, LLC, uses activity-based costing to allocate variable manufacturing overhead costs to products. The company identified three activities with the following information for last month.

| Activity | Standard Rate | Standard Quantity per Unit Produced | Actual Costs | Actual Quantity |

| Purchase orders | $50 per order | 0.10 order per unit | $65,000 | 1,600 orders |

| Product testing | $2 per test minute | 0.50 minutes per unit | $17,000 | 8,000 test minutes |

| Indirect labor | $3 per direct labor hour | 1 hour per unit | $43,000 | 13,000 direct labor hours |

Required:

Assume Hillside Hats produced 15,000 units last month. Prepare a variance analysis using the format shown in Figure 10.11 "Variable Overhead Variance Analysis for Jerry’s Ice Cream Using Activity-Based Costing". Clearly label each variance as favorable or unfavorable.

Closing Variance and Overhead Accounts (Appendix). Shasta Company had the following balances at the end of its fiscal year.

| Debit | Credit | |

| Materials price variance | $8,000 | |

| Materials quantity variance | 2,000 | |

| Labor rate variance | $12,000 | |

| Labor efficiency variance | 5,000 | |

| Manufacturing overhead | 4,000 |

Required:

Problems

Variance Analysis for Direct Materials, Direct Labor, and Variable Overhead. Rain Gear, Inc., produces rain jackets. The master budget shows the following standards information and indicates the company expected to produce and sell 28,000 units for the year.

| Direct materials | 4 yards per unit at $3 per yard |

| Direct labor | 2 hours per unit at $10 per hour |

| Variable manufacturing overhead | 2 direct labor hours per unit at $4 per hour |

Rain Gear actually produced and sold 30,000 units for the year. During the year, the company purchased 130,000 yards of material for $429,000 and used 118,000 yards in production. A total of 65,000 labor hours were worked during the year at a cost of $637,000. Variable overhead costs totaled $231,000 for the year.

Required:

Fixed Overhead Variance Analysis. (This problem is a continuation of the previous problem but can also be worked independently.) Rain Gear, Inc., produces rain jackets and applies fixed manufacturing overhead costs to products based on direct labor hours. Information for the year appears as follows. Rain Gear expected to produce and sell 28,000 units for the year.

Required:

Journalizing Direct Materials, Direct Labor, and Overhead Transactions (Appendix). Complete the following requirements for Rain Gear, Inc., using your solutions to the previous two problems.

Required:

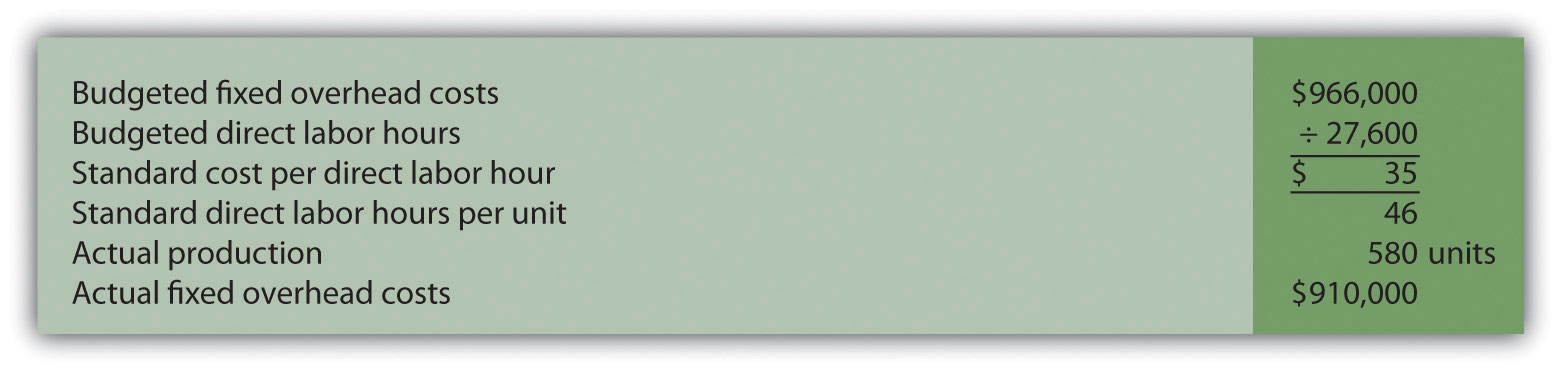

Variance Analysis for Direct Materials, Direct Labor, and Variable Overhead; Journalizing Direct Materials and Direct Labor Transactions (Includes Appendix). Prefab Pools Company produces large prefabricated in-ground swimming pools made of a specialized plastic material. The master budget shows the following standards information and indicates the company expected to produce and sell 600 units for the month of April.

| Direct materials | 500 pounds per unit at $7 per pound |

| Direct labor | 46 hours per unit at $12 per hour |

| Variable manufacturing overhead | 46 direct labor hours per unit at $30 per hour |

Prefab Pools actually produced and sold 580 units for the month. During the month, the company purchased 330,000 pounds of material for $2,277,000 and used 295,800 pounds in production. A total of 25,520 labor hours were worked during the month at a cost of $313,896. Variable overhead costs totaled $790,000 for the month.

Required:

Fixed Overhead Variance Analysis. (This problem is a continuation of the previous problem but can be worked independently.) Prefab Pools Company produces prefabricated in-ground swimming pools and applies fixed manufacturing overhead costs to products based on direct labor hours. Information for the month of April appears as follows. Prefab Pools expected to produce and sell 600 units for the month.

Required:

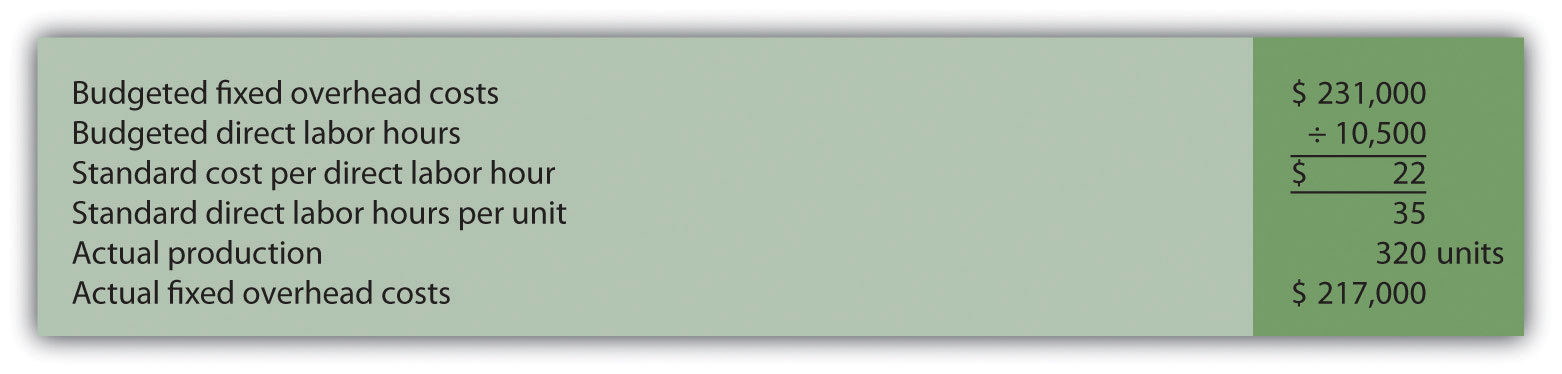

Variance Analysis for Direct Materials, Direct Labor, Variable Overhead, and Fixed Overhead. Equipment Products, Inc., produces large ladders made of a specialized metal material. The master budget shows the following standards information and indicates the company expected to produce and sell 4,000 units for the month of May.

| Direct materials | 60 pounds per unit at $3 per pound |

| Direct labor | 8 hours per unit at $14 per hour |

| Variable manufacturing overhead | 8 direct labor hours per unit at $6 per hour |

Equipment Products actually produced and sold 4,400 units for the month. During the month, the company purchased 300,000 pounds of material for $960,000 and used 286,000 pounds in production. A total of 30,800 labor hours were worked during the month at a cost of $462,000. Variable overhead costs totaled $195,000 for the month.

With regards to fixed manufacturing overhead, the company also applies these overhead costs to products based on direct labor hours. Fixed manufacturing overhead information for the month of May appears as follows.

Required:

Journalizing Direct Labor and Overhead Transactions (Appendix). Complete the following requirements for Equipment Products, Inc., using your solutions to the previous problem.

Required:

Variance Analysis with Activity-Based Costing. Assume Spindle Company uses activity-based costing to allocate variable manufacturing overhead costs to products. The company identified three activities with the following information for last quarter.

| Activity | Standard Rate | Standard Quantity per Unit Produced | Actual Costs | Actual Quantity |

| Indirect materials | $5 per yard | 14 yards per unit | $4,850,000 | 990,000 yards |

| Product testing | $3 per test minute | 10 minutes per unit | $2,000,000 | 650,000 test minutes |

| Indirect labor | $9 per direct labor hour | 6 hours per unit | $3,800,000 | 410,000 direct labor hours |

Required:

One Step Further: Skill-Building Cases

Group Activity: Setting Standards. Form groups of two to four students. Each group is to complete the following requirements.

Required:

Ethics and Setting Standards. Wilkes Golf, Inc., produces golf carts that are sold throughout the world. The company’s management is in the process of establishing the standard hours of direct labor required to complete one golf cart. Assume you are the production supervisor, and you receive a bonus for each quarter that shows a favorable labor efficiency variance. That is, you receive a bonus for each quarter showing actual direct labor hours that are fewer than budgeted direct labor hours.

The management has asked for your input in establishing the standard number of direct labor hours required to complete one golf cart.

Required:

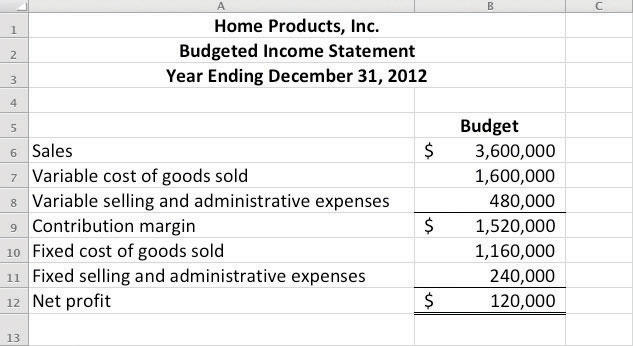

Using Excel to Perform Budget Versus Actual Analysis. The management of Home Products, Inc., prepared the following budgeted income statement for the year ending December 31, 2012.

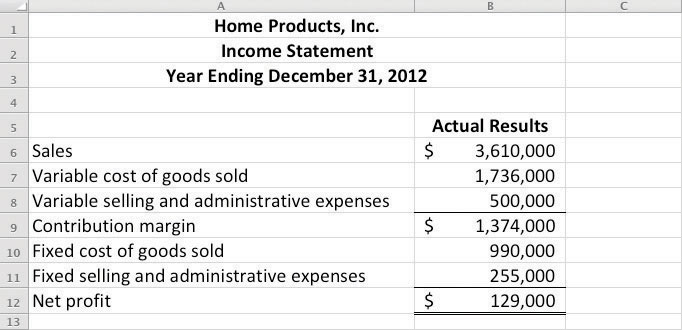

At the end of 2012, the company prepared the following income statement showing actual results:

Required:

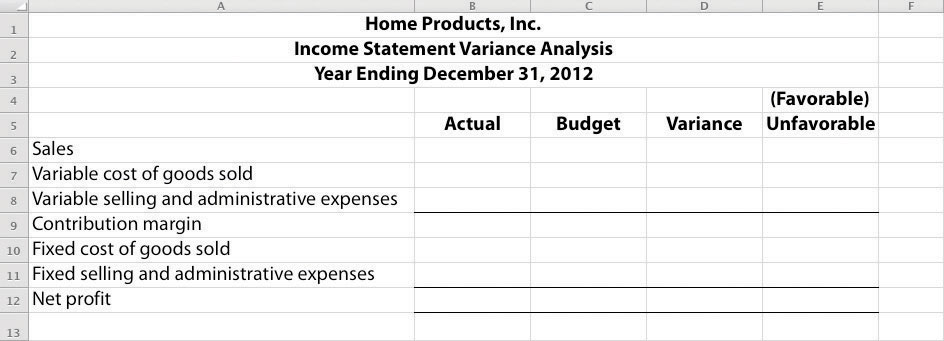

Prepare an Excel spreadsheet comparing the actual results to budgeted amounts using the format shown as follows, and comment on the results.

Comprehensive Cases

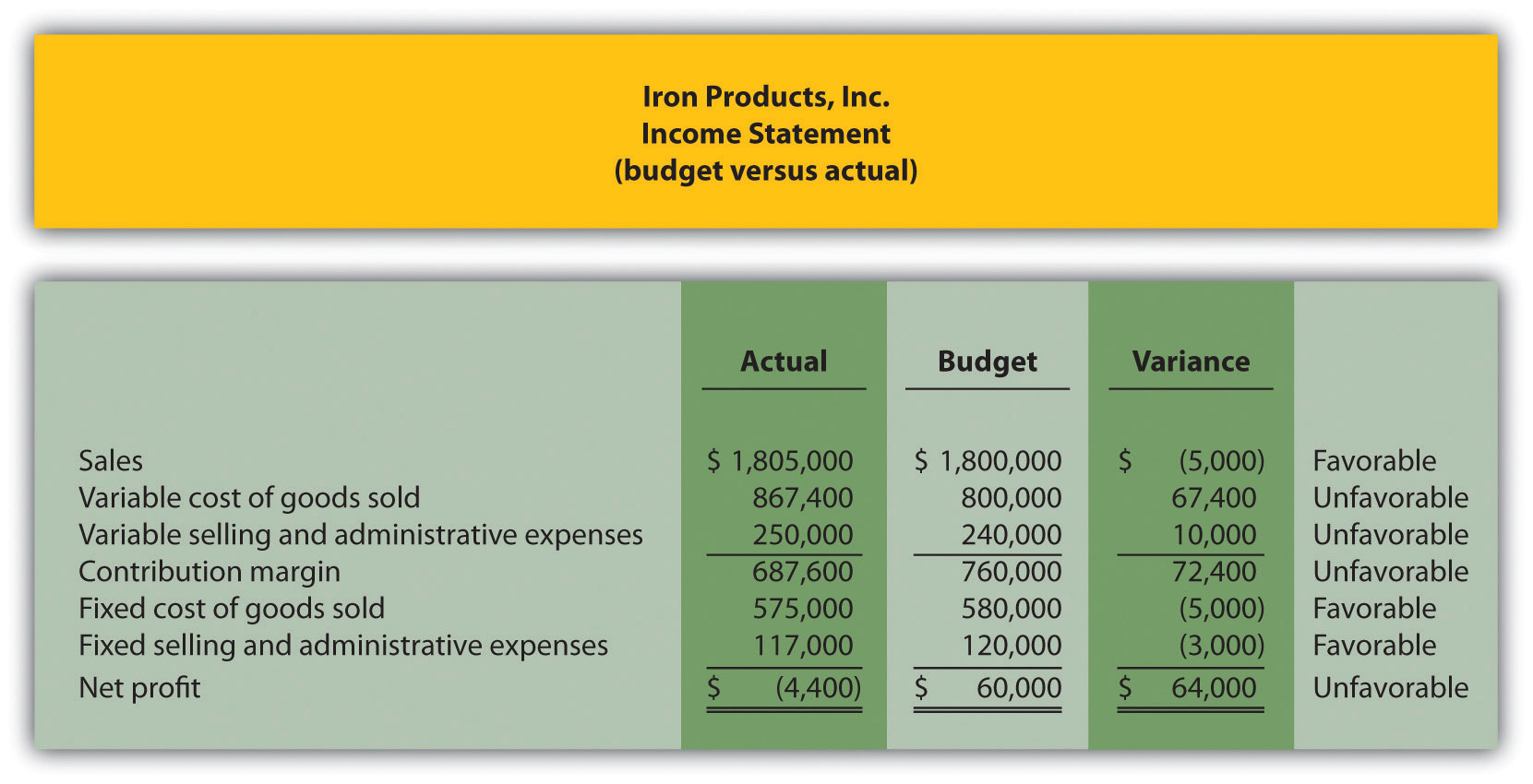

Variable Production Cost Variance Analysis. Iron Products, Inc., produces prefabricated iron fencing used in commercial construction. Variable overhead is applied to products based on direct labor hours. The company uses a just-in-time production system and thus has insignificant inventory levels at the end of each month. The income statement for the month of November comparing actual results with the flexible budget based on actual sales of 2,000 units is shown as follows.

Iron Products is disappointed with the actual results and has hired you as a consultant to provide further information as to why the company has been struggling to meet budgeted net profit. Your review of the previously presented budget versus actual analysis identifies variable cost of goods sold as the main culprit. The unfavorable variance for this line item is $67,400.

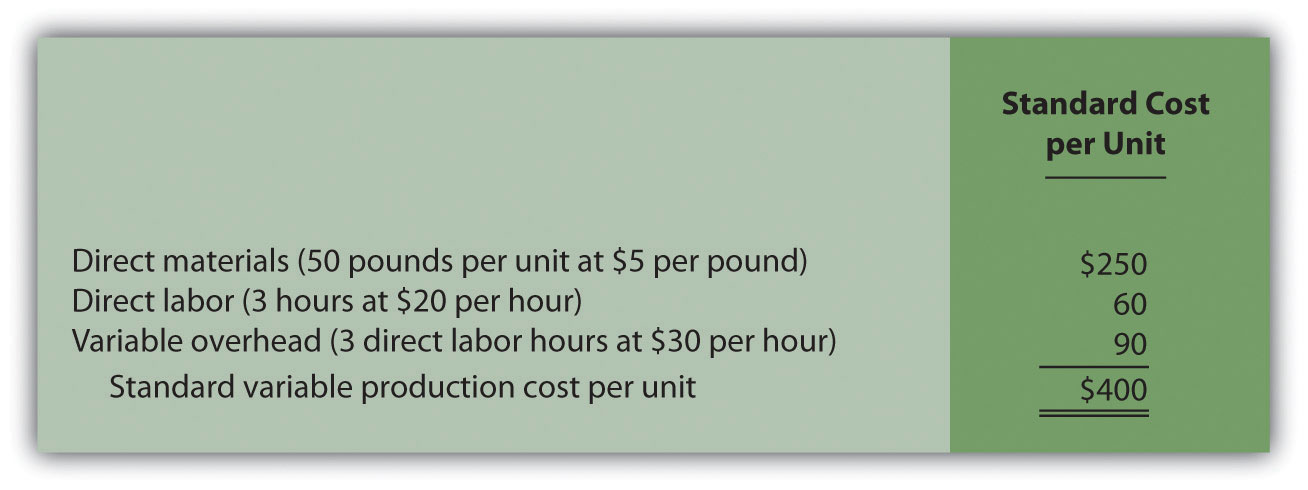

After further research, you are able to track down the following standard cost information for variable production costs:

Actual production information related to variable cost of goods sold for the month of November is as follows:

Required:

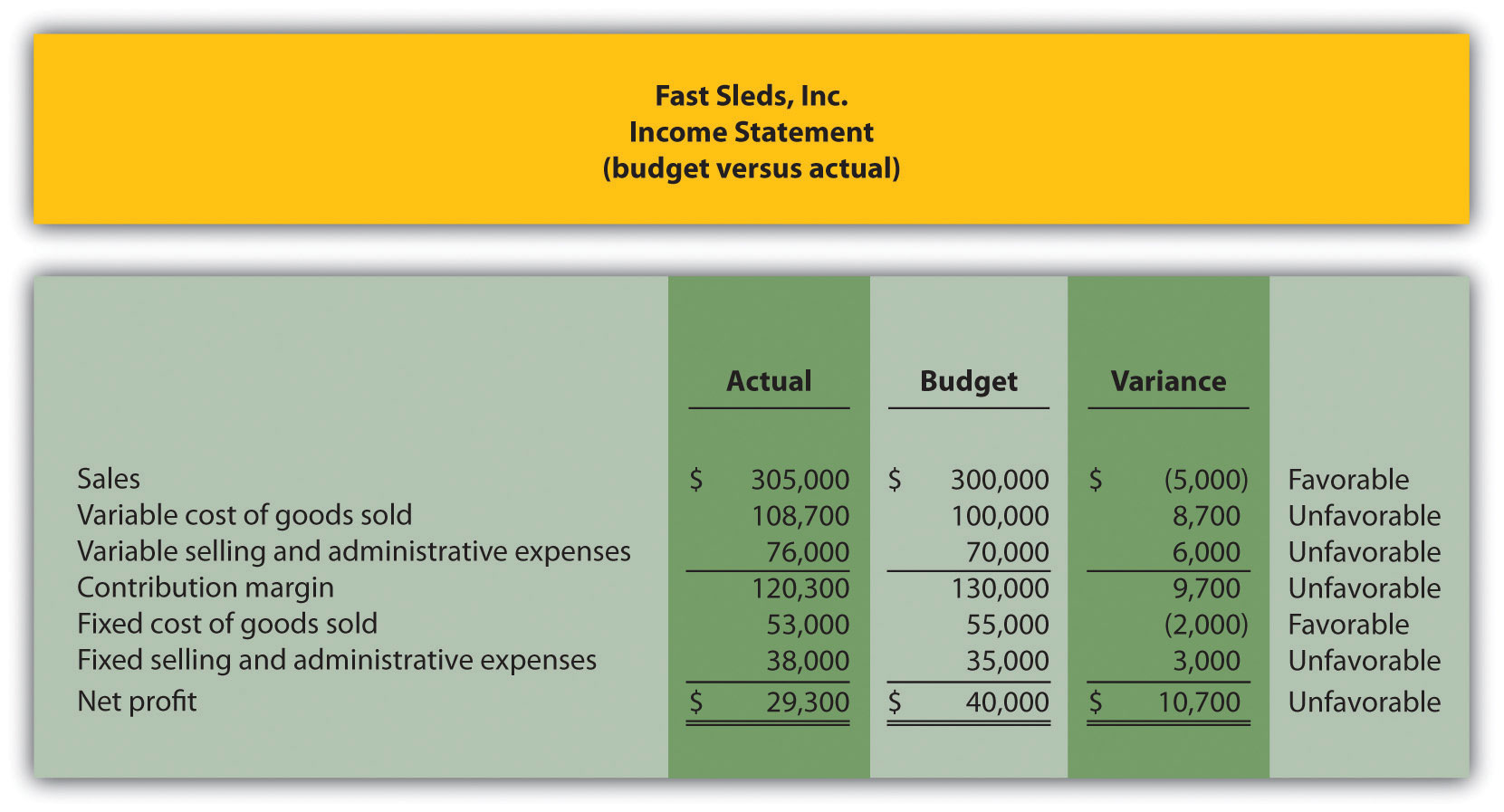

Variable Production Cost Variance Analysis and Performance Evaluation. Fast Sleds, Inc., produces snow sleds used for winter recreation. Variable overhead is applied to products based on machine hours. The company uses a just-in-time production system, and thus has insignificant inventory levels at the end of each month. The income statement for the month of January comparing actual results with the flexible budget is shown in the following based on actual sales of 10,000 units.

Fast Sleds is disappointed with the actual results and has hired you as a consultant to provide further information as to why the company has been struggling to meet budgeted net income. Your review of the budget presented previously versus actual analysis identifies variable cost of goods sold as the main culprit. The unfavorable variance for this line item is $8,700.

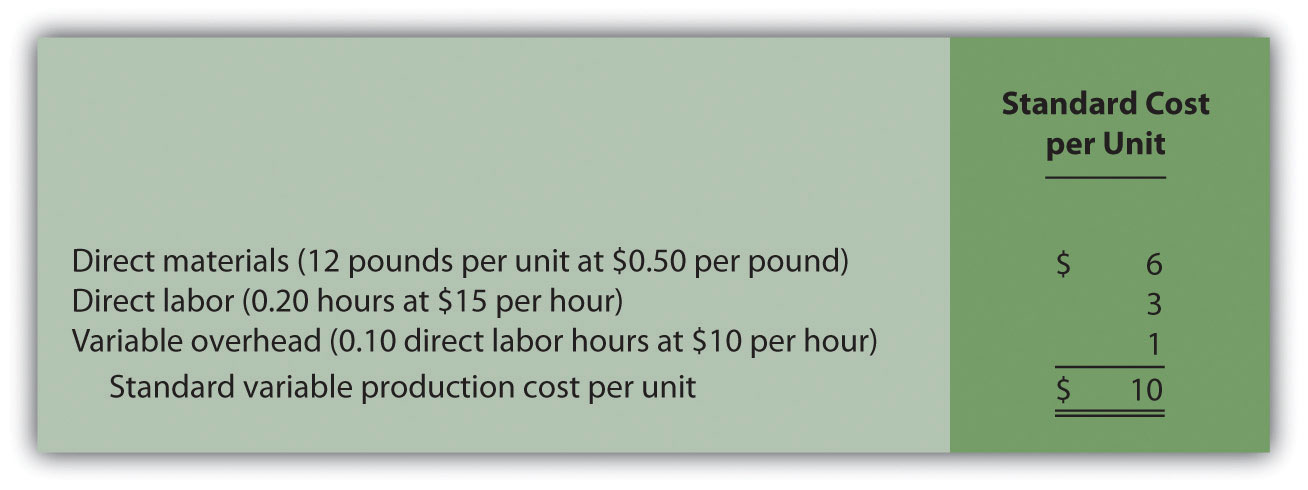

After further research, you are able to track down the standard cost information for variable production costs:

Actual production information related to variable cost of goods sold for the month of January is as follows:

Required: