This chapter examined the world of imperfect competition that exists between the idealized extremes of perfect competition and monopoly. Imperfectly competitive markets exist whenever there is more than one seller in a market and at least one seller has some degree of control over price.

We discussed two general types of imperfectly competitive markets: monopolistic competition and oligopoly. Monopolistic competition is characterized by many firms producing similar but differentiated goods and services in a market with easy entry and exit. Oligopoly is characterized by relatively few firms producing either standardized or differentiated products. There may be substantial barriers to entry and exit.

In the short run, a monopolistically competitive firm’s pricing and output decisions are the same as those of a monopoly. In the long run, economic profits will be whittled away by the entry of new firms and new products that increase the number of close substitutes. An industry dominated by a few firms is an oligopoly. Each oligopolist is aware of its interdependence with other firms in the industry and is constantly aware of the behavior of its rivals. Oligopolists engage in strategic decision making in order to determine their best output and pricing strategies as well as the best forms of nonprice competition.

Advertising in imperfectly competitive markets can increase the degree of competitiveness by encouraging price competition and promoting entry. It can also decrease competition by establishing brand loyalty and thus creating barriers to entry.

Where conditions permit, a firm can increase its profits by price discrimination, charging different prices to customers with different elasticities of demand. To practice price discrimination, a price-setting firm must be able to segment customers that have different elasticities of demand and must be able to prevent resale among its customers.

In the following list of goods and services, determine whether the item is produced under conditions of monopolistic competition or of oligopoly.

Suppose the monopolistically competitive barber shop industry in a community is in long-run equilibrium, and that the typical price is $20 per haircut. Moreover, the population is rising.

Consider the same industry as in Problem 1. Suppose the market is in long-run equilibrium and that an annual license fee is imposed on barber shops.

Industry A consists of four firms, each of which has an equal share of the market.

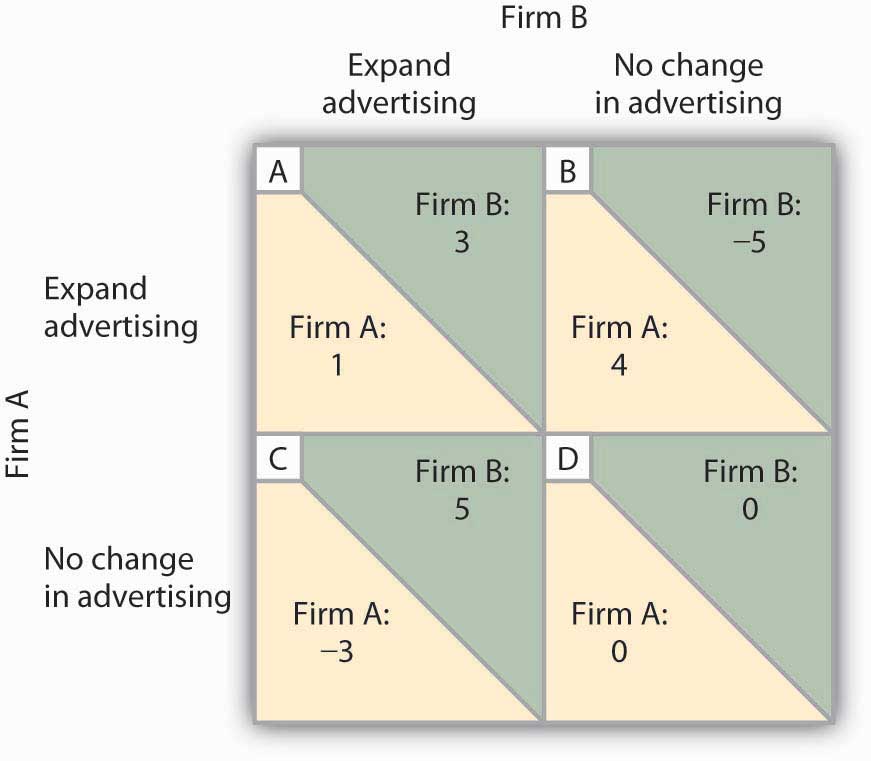

Given the payoff matrix (shown below) for a duopoly, consisting of Firm A and Firm B, in which each firm is considering an expanded advertising campaign, answer the following questions (all figures in the payoff matrix give changes in annual profits in millions of dollars):

Suppose that two industries each have a four-firm concentration ratio of 75%.

Suppose that a typical firm in a monopolistically competitive industry faces a demand curve given by:

q = 60 − (1/2)p, where q is quantity sold per week.The firm’s marginal cost curve is given by: MC = 60.