In the first three chapters, we provided information to help you understand and measure risks, as well as to evaluate risk attitudes and risk behavior. Chapter 4 "Evolving Risk Management: Fundamental Tools" concentrated on risk management and methods for identifying, measuring, and managing risks. In this chapter we elaborate further on the management of risk, placing greater emphasis on the opportunities that risk represents. We emphasize prudent opportunities rather than actions motivated by greed. When trying to identify the main causes of the 2008–2009 credit crisis, the lack of risk management and prudent behavior emerge as key factors. However, even companies that were not part of the debacle are paying the price, as the whole economy suffers a lack of credit and consumers’ entrenchment. Consumers are less inclined to buy something that they don’t consider a necessity. As such, even firms with prudent and well-organized risk management are currently seeing huge devaluation of their stocks.See explanation at http://www.Wikiperdia.org. see also “Executive Suite: Textron CEO Zeroes in on Six Sigma,” USA Today, updated January 28, 2008.

In many corporations, the head of the ERM effort is the chief risk officer or CRO. In other cases, the whole executive team handles the risk management decision with specific coordinators. Many large corporations adopted a system called Six Sigma, which is a business strategy widely adopted by many corporations to improve processes and efficiency. Within this model of operation they embedded enterprise risk management. The ERM function at Textron follows the latter model. Textron’s stock fell from $72 in January 2008 to $15 in December 2008. Let’s recall that ERM includes every aspect of risks within the corporation, including labor negotiation risks, innovation risks, lack-of-foresight risks, ignoring market condition risks, managing self-interest and greed risks, and so forth. Take the case of the three U.S. auto manufacturers—GM, Chrysler, and Ford. Their holistic risks include not only insuring buildings and automobiles or worker’s compensation. They must look at the complete picture of how to ensure survival in a competitive and technologically innovative world. The following is a brief examination of the risk factors that contributed to the near-bankrupt condition of the U.S. automakers: Paul Ingrassia, “How Detroit Drove into a Ditch: The Financial Crisis Has Brought the U.S. Auto Industry to a Breaking Point, but the Trouble Began Long Ago,” Wall Street Journal, October 25, 2008.

Had risk management been a top priority for the automobile companies, perhaps they would face a different attitude as they approach U.S. taxpayers for their bailouts. ERM needs to be part of the mind-set of every company stakeholder. When one arm of the company is pulling for its own gains without consideration of the total value it delivers to stakeholders, the result, no doubt, will be disastrous. The players need to dance together under the paradigm that every action might have the potential to lead to catastrophic results. The risk of each action needs to be clear, and assuredness for risk mitigation is a must.

This chapter includes the following:

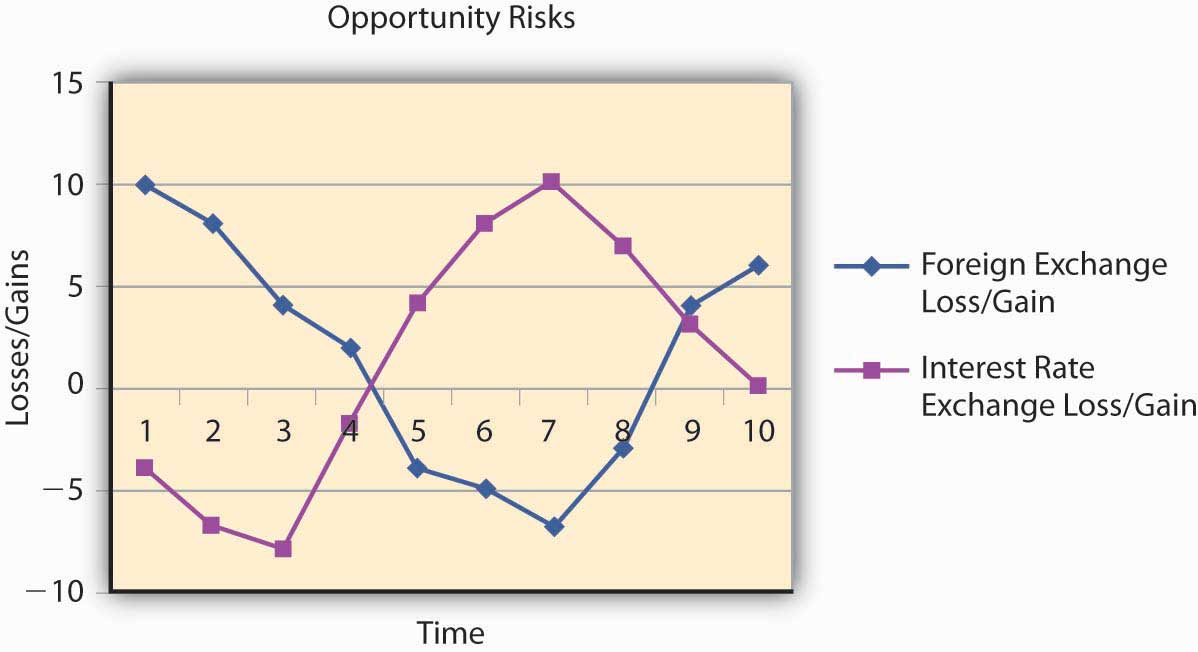

While Chapter 4 "Evolving Risk Management: Fundamental Tools" enumerated all risks, we emphasized the loss part more acutely, since avoiding losses represents the essence of risk management. But, with the advent of ERM, the risks that represent opportunities for gain are clearly just as important. The question is always “How do we evaluate activities in terms of losses and gains within the firm’s main goal of value maximization?” Therefore, we are going to look at maps that examine both sides—both gains and losses as they appear in Figure 5.1 "The Links to ERM with Opportunities and Risks". We operate on the negative and positive sides of the ERM map and we look into opportunity risks. We expand our puzzle to incorporate the firm’s goals. We introduce more sophisticated tools to ensure that you are equipped to work with all elements of risk management for firms to sustain themselves.

Figure 5.1 The Links to ERM with Opportunities and Risks

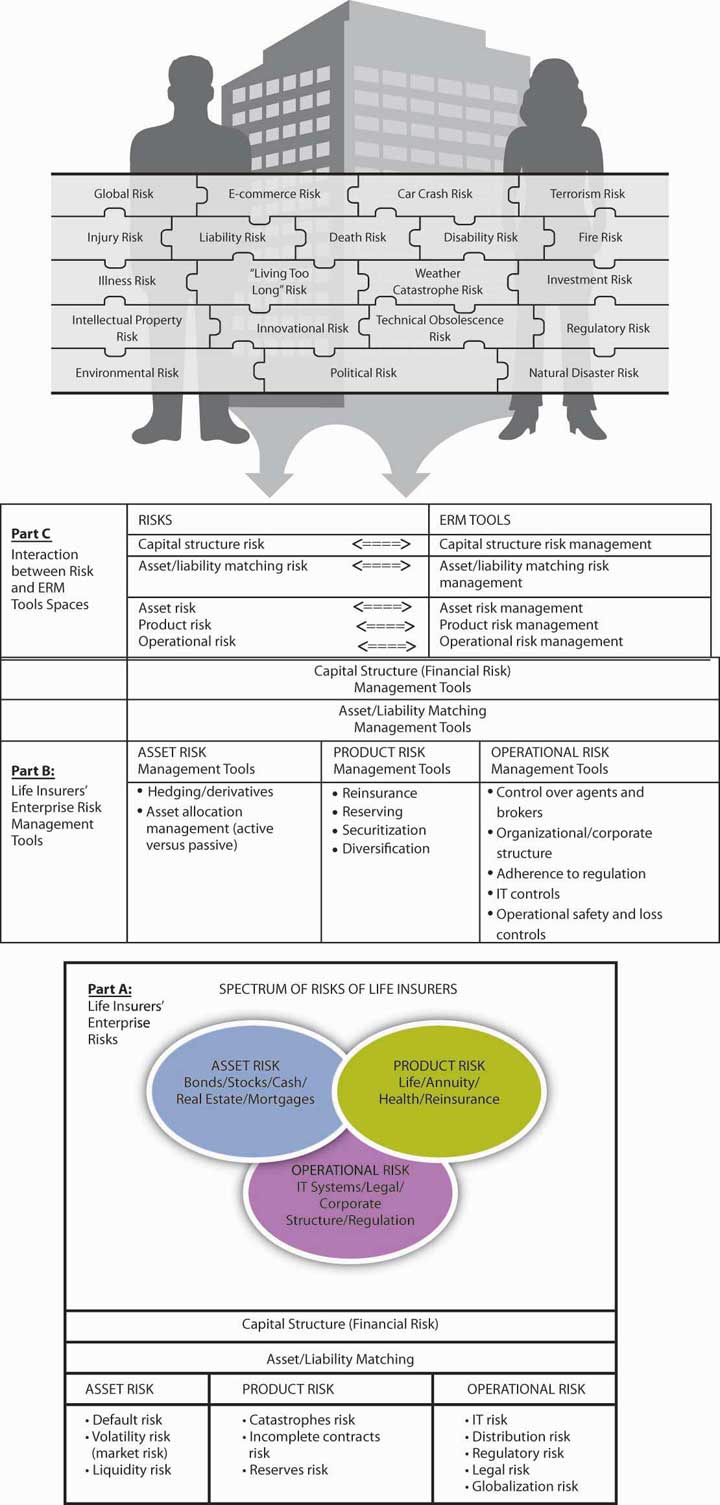

Let us emphasize that, in light of the financial crisis of 2008–2009, ERM is a needed mind-set for all disciplines. The tools are just what ERM-oriented managers can pull out of their tool kits. For example, we provide an example for the life insurance industry as a key to understanding the links. We provide a more complete picture of ERM in Figure 5.2 "Links between the Holistic Risk Picture and Conventional Risk and ERM Tools".

Figure 5.2 Links between the Holistic Risk Picture and Conventional Risk and ERM Tools

Part C illustrates the interaction between parts A and B.

Source: Etti G. Baranoff and Thomas W. Sager, “Integrated Risk Management in Life Insurance Companies,” a $10,000 award-winning paper, International Insurance Society Seminar, Chicago, July 2006 and in special edition of the Geneva Papers on Risk and Insurance Issues and Practice.