When insurers or risk managers use frequency and severity to project the future, they use trending techniques that apply to the loss distributions known to them.Forecasting is part of the Associate Risk Manager designation under the Risk Assessment course using the book: Baranoff Etti, Scott Harrington, and Greg Niehaus, Risk Assessment (Malvern, PA: American Institute for Chartered Property Casualty Underwriters/Insurance Institute of America, 2005). Regressions are the most commonly used tools to predict future losses and claims based on the past. In this textbook, we introduce linear regression using the data featured in Chapter 2 "Risk Measurement and Metrics". The scientific notations for the regressions are discussed later in this appendix.

Table 4.5 Linear Regression Trend of Claims and Losses of A

| Year | Actual Fire Claims | Linear Trend For Claims | Actual Fire Losses | Linear Trend For Losses |

|---|---|---|---|---|

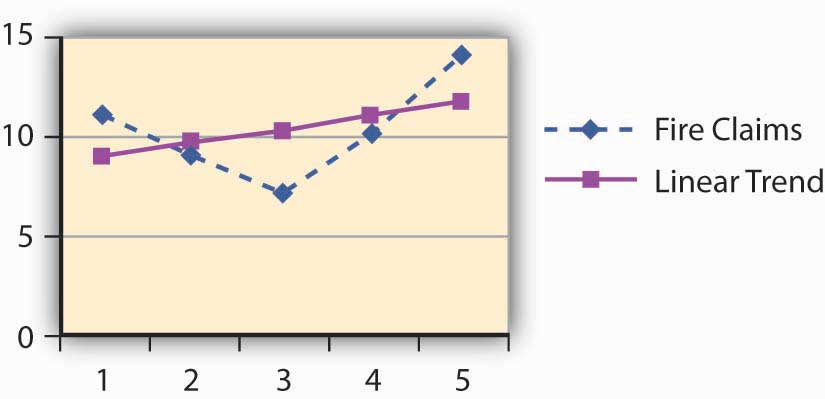

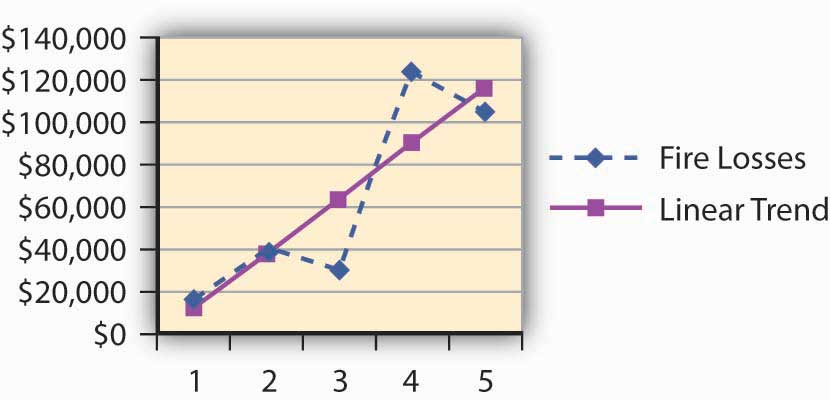

| 1 | 11 | 8.80 | $16,500 | $10,900.00 |

| 2 | 9 | 9.50 | $40,000 | $36,900.00 |

| 3 | 7 | 10.20 | $30,000 | $62,900.00 |

| 4 | 10 | 10.90 | $123,000 | $88,900.00 |

| 5 | 14 | 11.60 | $105,000 | $114,900.00 |

Figure 4.5 Linear Regression Trend of Claims of A

Figure 4.6 Linear Regression Trend of Losses of A

Linear regression attempts to explain the relationship among observed values by applying a straight line fit to the data. The linear regression model postulates that

,where the “residual” e is a random variable with mean of zero. The coefficients a and b are determined by the condition that the sum of the square residuals is as small as possible. For our purposes, we do not discuss the error term. We use the frequency and severity data of A for 5 years. Here, we provide the scientific notation that is behind Figure 4.5 "Linear Regression Trend of Claims of A" and Figure 4.6 "Linear Regression Trend of Losses of A".

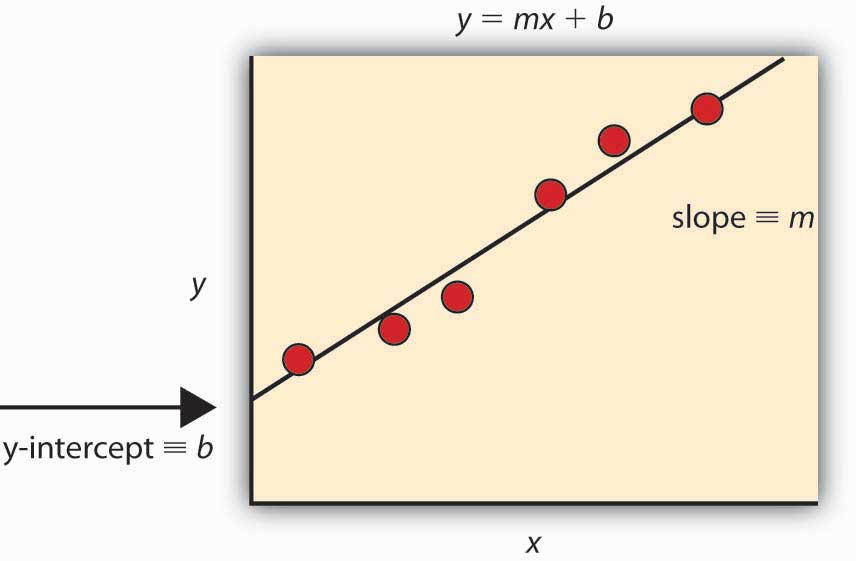

In order to determine the intercept of the line on the y-axis and the slope, we use m (slope) and b (y-intercept) in the equation.

Given a set of data with n data points, the slope (m) and the y-intercept (b) are determined using:

Figure 4.7 Showing the Slope and Intercept

The graph is provided by Chris D. Odom, with permission.

Most commonly, practitioners use various software applications to obtain the trends. The student is invited to experiment with Microsoft Excel spreadsheets. Table 4.6 "Method of Calculating the Trend Line for the Claims" provides the formulas and calculations for the intercept and slope of the claims to construct the trend line.

Table 4.6 Method of Calculating the Trend Line for the Claims

| (1) | (2) | (3) = (1) × (2) | (4) = (1)2 | ||

|---|---|---|---|---|---|

| Year | Claims | ||||

| X | Y | XY | X2 | ||

| 1 | 11 | 11.00 | 1 | ||

| 2 | 9 | 18.00 | 4 | ||

| 3 | 7 | 21.00 | 9 | ||

| 4 | 10 | 40.00 | 16 | ||

| n=5 | 14 | 70.00 | 25 | ||

| Total | 15 | 51 | 160 | 55 | |

| M = Slope = 0.7 | = | ||||

| b = Intercept = 8.1 | |||||

Future Forecasts using the Slopes and Intercepts for A:

The in-depth statistical explanation of the linear regression model is beyond the scope of this course. Interested students are invited to explore statistical models in elementary statistics textbooks. This first exposure to the world of forecasting, however, is critical to a student seeking further study in the fields of insurance and risk management.